Let's be honest, tax jargon can feel like another language. But franking credits are actually a straightforward concept. Think of them as a tax voucher that comes attached to the dividends you get from Australian companies.

It's basically proof that the company has already paid tax on its profits before sharing them with you. This whole system exists to stamp out a major headache for investors: double taxation.

Understanding Franking Credits in Simple Terms

Here's how it used to work: a company makes a profit and pays corporate tax to the Australian Taxation Office (ATO). Then, it distributes the leftover profit to you, the shareholder, as a dividend. You would then have to pay personal income tax on that same dividend.

See the problem? The same dollar of profit gets taxed twice. That’s not fair, and it’s not smart for the economy.

The Australian imputation system was brought in to fix this. It’s designed to make sure company profits are only taxed once, at the shareholder's individual tax rate.

How Does This Work in Practice?

A franking credit is like a pre-paid tax receipt. When a company pays you a dividend, it can attach a credit that shows how much tax it has already paid on your behalf. This is what we call a franked dividend.

When you do your tax return, you declare both the dividend amount and the attached franking credit as part of your income. The value of that credit is then used to reduce your final tax bill.

A franking credit acts as an offset against your personal income tax liability, acknowledging the corporate tax that has already been paid on your behalf.

It's a simple idea, but it has a huge impact on investment returns.

The Impact on Your Tax Bill

What this means for your wallet comes down to one thing: how your personal marginal tax rate stacks up against the company tax rate (which is usually 30%).

There are three possible outcomes:

- You may pay less tax: If your personal tax rate is higher than 30%, the franking credit covers a chunk of your tax bill, and you may only need to pay the difference.

- You may pay no more tax: If your tax rate is the same as the company's, the credit may cover your entire tax liability for that dividend.

- You may get a tax refund: This is the best bit. If your tax rate is lower than the company's, the ATO may refund you the difference in cash.

This system is why investing in Australian shares can be so attractive, particularly for people in lower tax brackets like retirees. It turns a standard dividend payment into a much more tax-effective stream of income.

Why Australia Created the Dividend Imputation System

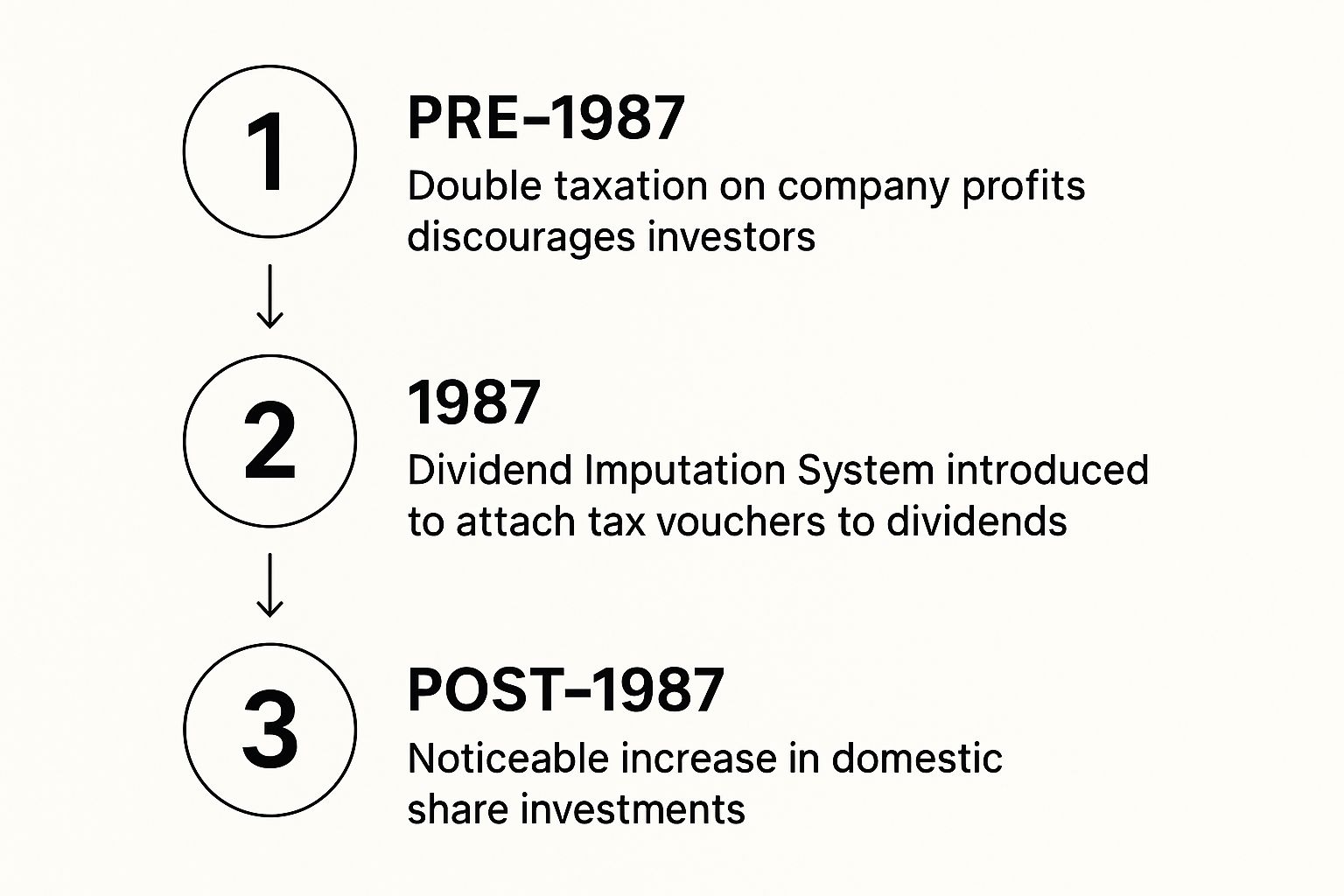

To really get your head around franking credits, it helps to take a quick trip back in time. Before 1987, the investing world in Australia was a very different place, and a big problem called double taxation was stopping everyday Aussies from backing local companies.

Here’s how it worked back then: Imagine a company made a profit. First, it paid company tax on those earnings. Fair enough. But then, when it shared the leftover profits with its shareholders as dividends, those shareholders had to pay personal income tax on that exact same money.

Essentially, the same dollar of profit was getting taxed twice. This was not only unfair, but it was also a massive roadblock for the economy. It slashed the real returns for investors and made putting money into Australian businesses a lot less attractive than, say, investing in property. The government knew something had to change.

A Fairer System for All

The solution that landed was the dividend imputation system, a game-changing tax reform introduced in 1987. The whole point was to get people excited about investing in Australian companies by making the tax system fairer and more efficient.

The core idea is simple: make sure company profits are only taxed once, at the shareholder's personal tax rate. If you're keen on the nitty-gritty of this policy shift, the Parliamentary Budget Office has a great explainer on dividend imputation.

This wasn't just a minor tweak; it became a cornerstone of Australia's investment philosophy. By killing off double taxation, it completely changed the game for both companies and investors, shaping the financial markets we know today.

The infographic below really paints a clear picture of this policy shift and what it was designed to achieve.

As you can see, the imputation system was a direct answer to the problem of double taxation, creating a much more appealing environment for people to own shares in local businesses.

The Lasting Impact on Investors

So, where do franking credits fit in? They're the little "vouchers" that make this whole system work. They act as proof that company tax has already been paid on a dividend, allowing shareholders to use that credit to reduce their own tax bill.

This single reform made investing in Australian shares far more attractive. It encouraged money to flow into local businesses, which in turn helped support the country's economic growth.

Understanding this history is crucial. Franking credits aren't just some obscure tax rule; they are a foundational part of how Australia approaches investment and corporate tax.

For small business owners and individual investors, understanding this concept is a key piece of managing finances effectively. Staying on top of your obligations is essential, and you can find more practical information in our articles on tax and compliance for businesses. This historical context shows just how important it is to manage dividends and credits properly.

A Practical Walkthrough of How Franking Credits Work

The theory is one thing, but seeing franking credits in action is where it all clicks. Let's follow a single dollar of profit from a hypothetical Aussie company, "AusCo Pty Ltd," and see how it makes its way into your bank account.

Imagine AusCo has a great year and earns $100 in profit for every share. Before it can pass this on to shareholders, it has to pay company tax. With the corporate tax rate at 30%, AusCo sends $30 to the ATO. That leaves $70 in after-tax profit.

The company decides to pay out that entire remaining $70 as a dividend. Because it already paid $30 in tax on that original profit, it can attach a $30 franking credit to the dividend. This is what we call a fully franked dividend.

The Shareholder's Perspective

Now, let's switch over to your side of the table as the investor. When you sit down to do your tax return, you don’t just declare the $70 cash dividend you received. You report the "grossed-up" dividend, which is the cash amount plus the franking credit.

The grossed-up dividend shows the full pre-tax profit your share of the company actually earned. In this case, you’d declare $100 ($70 cash + $30 franking credit) as assessable income from this investment.

This gross-up step is crucial because it ensures the profit is taxed at your personal marginal tax rate, with the franking credit acting like a tax pre-payment. The final outcome all comes down to how your tax rate stacks up against the 30% the company already paid. If you want to dig deeper into the mechanics, you can discover additional insights about franked income on betashares.com.au.

Franking Credits in Action: Shareholder Tax Outcomes

The real magic of the imputation system shines through when we compare three different investors, each with a different marginal tax rate. All three receive the same $70 cash dividend with the same $30 franking credit.

This table breaks down exactly what happens for each of them.

| Shareholder Scenario | Marginal Tax Rate | Grossed-Up Dividend | Tax on Dividend | Franking Credit Applied | Final Outcome (Refund/Tax Payable) |

|---|---|---|---|---|---|

| Investor A (Low Rate) | 19% | $100 | $19 | $30 | $11 Refund |

| Investor B (Mid Rate) | 30% | $100 | $30 | $30 | $0 Tax Payable |

| Investor C (High Rate) | 45% | $100 | $45 | $30 | $15 Tax Payable |

Let's look at what the table tells us:

-

Investor A, who is on a low 19% tax rate, only owed $19 in tax on the profit. Since $30 was already paid by AusCo, the ATO gives them back the $11 difference. That’s a cash refund.

-

Investor B's personal tax rate of 30% is a perfect match for the company tax rate. The $30 franking credit covers their entire tax bill, so they have zero to pay and nothing to get back.

-

Investor C is a high-income earner on a 45% tax rate, meaning their tax liability is $45. The $30 credit takes care of most of this, but they still need to chip in the remaining $15.

As you can see, the system works to ensure fairness. Instead of profits being taxed once at the company level and again at the shareholder level, they’re taxed just once at the investor's correct marginal rate. Franking credits are simply the mechanism that makes it all square up.

How Franking Credits Boost Your Investment Returns

Franking credits are a lot more than just a box to tick on your tax return; they're a powerful way to supercharge the returns from your investment portfolio. They have the effect of increasing the real, after-tax return you get from Australian shares, turning a decent dividend payment into a fantastic one. It's why dividend-paying Aussie stocks are such a popular cornerstone for income-focused investors.

The dividend yield you see advertised for a stock really only tells you half the story. The true value comes into focus when you look at the "grossed-up" yield, which is just a fancy way of saying the dividend plus the franking credit. Over time, that extra kick can make a huge difference to your wealth-building journey.

Think about it this way: a share with a 4.5% dividend yield might seem okay, but not exactly thrilling. But once you add the franking credits to the equation, its effective yield can jump to over 6%. That's a serious lift that directly impacts your total return.

Putting a Number on the Impact

This isn’t just a small perk; it's a major driver of the total return you get from the Aussie stock market. When dividend yields are otherwise a bit low, franking credits really shine. Data from the ATO backs this up, showing that while average dividend yields have hovered around 4% to 5% in recent years, franking credits can tack on another 1.5% to 2%. Suddenly, that franked dividend is delivering a pre-tax equivalent yield of 6% to 7% — a number that puts you in a much better after-tax position. You can dive deeper into the official numbers by exploring the ATO's findings on franking credit yields.

This boost is especially potent for investors who are in lower tax brackets.

For many retirees and Self-Managed Superannuation Funds (SMSFs), franking credits go from being a simple tax offset to a direct source of cash flow, especially if their marginal tax rate is 0% or 15%.

A Game-Changer for Retirees and SMSFs

The benefits really kick into high gear for those with lower personal tax rates. Let's look at two of the biggest beneficiaries:

-

Retirees: Plenty of retirees have an income that sits below the tax-free threshold. When they receive a fully franked dividend, the tax credit attached is worth more than the tax they actually owe. The result? A straight-up cash refund from the ATO.

-

Self-Managed Superannuation Funds (SMSFs): An SMSF that's in the "pension phase" pays 0% tax on its investment earnings. This means it can claim back 100% of the value of any franking credits as a cash refund, providing a massive boost to the fund's income.

For these investors, franking credits are far from a footnote on a dividend statement. They represent a real, tangible cash injection that can support retirement income streams or grow the fund's capital. Getting your head around what franking credits are and how they work is one of the fundamentals of building a smart, tax-effective investment strategy in Australia.

Decoding Your Dividend Statement

When your dividend statement lands in your inbox or letterbox, it can feel like you’re trying to read a foreign language. But once you know the lingo, you can unlock the real value of your investment and make sure you’re reporting everything correctly. Think of this as your personal decoder ring for your investment paperwork.

These documents don’t just tell you how much cash you received; they also show how much pre-paid tax came along with it. Getting a handle on each term is essential, especially when tax time rolls around.

To make things a bit clearer, here's a quick rundown of the key terms you’ll come across on your dividend statements.

Franking Terminology Explained

This table breaks down the essential terms you'll encounter, what they mean in simple English, and why they matter to you.

| Term | Simple Definition | What It Means for You |

|---|---|---|

| Fully Franked | The company paid the full 30% corporate tax on its profit before paying your dividend. | This means you receive the maximum amount of tax credits with your dividend, which can significantly reduce your tax bill. |

| Partially Franked | The company only paid some Australian tax on the profit. | This means you get some tax credits, but not the full amount. This often happens if the company earns a lot of money overseas. |

| Unfranked | No Australian company tax was paid on the profit that generated the dividend. | There are no franking credits attached. You receive the cash, but no pre-paid tax benefit. |

| Gross-Up Amount | The cash dividend you received plus the value of the attached franking credits. | This is the total pre-tax value of your dividend. It's the amount you must declare as income to the ATO. |

Getting comfortable with this terminology is the first step to confidently managing your investment income. Let's dig a little deeper into what this looks like in practice.

Franking Status Explained

The first thing to look for is the franking status. This tells you a story about where the company's profits came from and how much tax has already been taken care of on your behalf.

You'll usually see one of three types:

-

Fully Franked: This is the one you want to see. It means the company paid the full corporate tax rate (typically 30%) on its profit before sending you your share. The dividend comes packed with the maximum possible franking credits.

-

Partially Franked: This means the company paid some tax in Australia, but not the full amount. It’s common for businesses with significant international operations, where they might have paid taxes to other governments instead.

-

Unfranked: This is straightforward—no Australian company tax was paid on the profit behind your dividend. Because of this, no franking credits are attached.

If you’re staring at your investment paperwork and it still feels overwhelming, it might be time to call in a professional. For business owners, understanding why every business needs an accountant is often the first step toward achieving this kind of financial clarity and peace of mind.

The Gross-Up Amount

Another key figure on your statement is the gross-up amount. It’s a simple but vital calculation: the cash dividend you received, plus the value of the franking credits.

The grossed-up dividend shows the full, pre-tax value of your share of the company's profit. This is the figure you must declare as assessable income on your tax return.

Let's make it real. Say you get a $70 cash dividend, and it comes with $30 in franking credits. Your grossed-up dividend is $100.

You then declare the full $100 as income to the ATO, and that $30 credit is used to directly reduce your final tax bill. This whole process is designed to make sure the profit is taxed just once, at your personal tax rate.

Claiming Franking Credits: A General Guide

Alright, so you’ve got your head around the theory of franking credits. Now for the fun part: seeing how it all works when you actually lodge your tax return. Getting those credits isn't complicated, but you do need to pay close attention to the details on your dividend statement.

Think of your dividend statement as the golden ticket. It’s the one document that lays out all the numbers you need, from the cash dividend you received to, most importantly, the value of the franking credit attached. This statement is your roadmap for telling the Australian Taxation Office (ATO) exactly what your investment earned.

The Reporting Process in a Nutshell

When you sit down to do your tax, you don’t just declare the cash that landed in your bank account. Instead, you need to report the ‘grossed-up’ dividend as part of your assessable income. This figure is simply the cash dividend plus the franking credit, representing the full pre-tax profit your shares generated for you.

Once you’ve declared that grossed-up amount, you then claim the franking credit as a tax offset. This is where the magic happens, as it directly reduces the tax you owe. It’s a simple two-step dance: declare the total profit, then subtract the tax the company already paid on your behalf.

Important Disclaimer: The information here is for general guidance only and should not be taken as financial or tax advice. The Australian tax system is a complex beast, and everyone's situation is different. We strongly recommend chatting with a registered tax agent to make sure you’re compliant and get advice that’s right for you.

Record Keeping and Professional Guidance

This probably goes without saying, but keeping good records is non-negotiable. File away all your dividend statements neatly and make sure they’re easy to find. They are the proof you need to back up your claims. Tidy record-keeping makes lodging your return a breeze and gives you a clear paper trail if the ATO ever comes knocking.

For many individuals and business owners, getting an expert to handle the numbers is the smartest move. The rules can be fiddly, which is why understanding how to navigate tax season with professional help can save you a world of stress. A good tax agent will make sure you claim every cent you're entitled to while keeping you squarely on the right side of the ATO.

Common Questions About Franking Credits

Even once you get your head around the basics, franking credits can throw up a lot of "what if" questions. Let's tackle some of the most common queries that pop up for investors, so you can handle the practical side of the imputation system with confidence.

Do All Australian Companies Pay Franked Dividends?

Not always, no. The key thing to remember is a company can only pass on franking credits if it has actually paid Australian corporate tax.

There are a few common reasons a business might pay out unfranked or only partially franked dividends:

- They might have had a tough year and incurred tax losses, meaning they didn't pay any corporate tax.

- A big chunk of their profits might have come from their overseas operations, which aren't subject to Australian tax.

- Sometimes, their specific corporate structure can affect their ability to generate franking credits to pass on.

What Is the 45-Day Holding Rule?

This one's a big deal. It’s a crucial rule the ATO put in place to stop people from gaming the system. To be eligible to claim franking credits, you generally need to hold the shares ‘at risk’ for at least 45 continuous days. This doesn't include the day you buy or sell them.

The rule is there to prevent a practice called ‘dividend stripping’. This is where an investor might swoop in to buy shares just before a dividend is announced, purely to grab the tax credit, and then sell them straight after.

Can I Get Franking Credits from International Shares?

That’s a definite no. Franking credits are a uniquely Australian thing. They are only ever attached to dividends from Australian resident companies that have paid Australian corporate tax.

So, you won't see them on your dividends from global giants like Microsoft or Apple. While you might be able to claim a foreign income tax offset if tax was withheld in another country, that's a completely different mechanism and has nothing to do with the Australian franking credit system.

Trying to navigate the finer points of franking credits, business reporting, and tax compliance can feel overwhelming. The team at Genesis Hub specialises in making finance simple for small businesses and investors, ensuring you stay compliant while making the most of your returns. Book a free consultation to strengthen your financial strategy today.