So, you’re thinking about setting up a trust in Australia. It’s a smart move for many business owners looking to protect assets and manage their wealth, but it’s not as simple as just filling out a form. At its heart, a trust is a formal relationship established by a legal document. It involves a trustee who manages assets for the people who will ultimately benefit, the beneficiaries.

The whole thing gets kicked off by a settlor, who provides the initial assets to get the trust up and running. Getting your head around these core pieces is the absolute first step.

First Steps in Setting Up Your Trust

Before you get lost in the legal documents, it’s really important to know that a trust isn’t a company or a partnership. Think of it as a fiduciary arrangement—a formal agreement where one party holds assets purely for the benefit of another. This isn’t just semantics; this distinction is fundamental to getting your trust set up correctly in Australia.

The entire structure hinges on the relationship between three key roles. If you get these roles right from day one, you’ll sidestep a world of future complications and make sure the trust actually does what you want it to.

The Key Players in Your Trust

Every single trust, no matter how simple or complex, has three distinct roles. Each one has a very specific job to do:

- The Settlor: This is the person or company that officially creates the trust. Their main task is to provide the initial asset—often just a token amount like $10—which is legally “settled” to bring the trust into existence. After that, the settlor bows out and can’t have any further involvement or get any benefit from the trust.

- The Trustee: This is the legal owner of the trust’s assets. They are responsible for managing everything according to the rules laid out in the trust deed. A trustee can be one or more people, but it’s often a company (known as a corporate trustee). They have a strict, legally binding duty to always act in the best interests of the beneficiaries.

- The Beneficiaries: These are the people or entities who will benefit from the trust’s assets and any income it generates. In a typical family trust, the beneficiaries are family members, but they can also be companies or even other trusts.

Imagine it like this: a parent (the settlor) gives a responsible older sibling (the trustee) some money to manage for their younger siblings (the beneficiaries). The older sibling has to manage that money wisely for the others, not for themselves.

A common and costly mistake is mixing up the roles of settlor and beneficiary. The settlor cannot be a beneficiary of the trust they create. This is a non-negotiable legal requirement for a valid trust in Australia.

Why This Structure Matters

Understanding this framework is the real first step because it defines the trust’s entire purpose. This isn’t just about paperwork; it’s about setting up clear duties and entitlements.

This legal separation of ownership (the trustee) from the actual benefit (the beneficiaries) is what makes a trust such a powerful tool for asset protection and managing wealth. Defining these roles properly from the get-go ensures your trust is legally sound and ready to help you achieve your financial goals. As you build these financial structures, getting expert advice is key, which is why every business needs an accountant to guide them.

Choosing the Right Trust Structure

Getting the right trust structure from the get-go is one of the most critical decisions you’ll make. It’s not just paperwork; the structure you choose has a direct line to how your assets are managed and, most importantly, how income gets distributed.

This isn’t a one-size-fits-all deal. Your business goals, family situation, and what you see on the horizon will all point you toward the right fit. While there are a few different types, most small business owners end up weighing up two main players: the discretionary trust (often just called a family trust) and the unit trust.

They each serve a completely different purpose, so let’s break them down with some real-world scenarios.

The Discretionary or Family Trust

The word you need to remember for a discretionary trust is flexibility. The trustee holds the power to decide which beneficiaries get a slice of the income or capital pie each financial year, and how big that slice is. This is exactly why they are the go-to choice for family-run businesses and managing family wealth.

Let’s say you run a small consulting business through a family trust. In a great year, the trustee might decide to distribute income to various beneficiaries based on their circumstances. This ability to adapt year-on-year is its biggest strength.

- Best for: Families who want to manage assets and stream income between members. It’s a powerhouse for asset protection and planning for the future.

- Key Feature: The trustee has complete discretion over distributions each year. Beneficiaries don’t have a fixed claim to any of the trust’s assets or income.

Just a heads-up: while this flexibility is fantastic, these decisions can have significant legal and financial consequences. The information provided here is for general educational purposes and is not a substitute for professional advice. Always have a chat with a qualified professional.

The Unit Trust

On the other end of the spectrum, a unit trust is all about fixed interests. Think of it like a company—the trust’s ownership is chopped up into “units,” just like shares. Each person who holds units is entitled to a fixed percentage of the trust’s income and capital, based purely on how many units they own.

If you hold 25% of the units, you get 25% of the distributions. Simple as that.

This rigid setup makes it a poor choice for a typical family structure but absolutely perfect for joint ventures between people who aren’t related. For example, if you and a business partner decide to buy a commercial property together, a unit trust spells out each person’s stake in black and white. There’s no room for arguments about who gets what.

- Best for: Unrelated business partners or investors who need their entitlements to income and capital clearly defined and locked in.

- Key Feature: Ownership is divided into units. Entitlements are directly tied to the number of units held, with zero trustee discretion on how distributions are paid out.

Discretionary Trust vs Unit Trust: A Comparison

To help make the choice a bit clearer, here’s a quick table breaking down the core differences between Australia’s two most common trust types.

| Feature | Discretionary (Family) Trust | Unit Trust |

|---|---|---|

| Income Distribution | Flexible; trustee decides each year. | Fixed; based on the number of units held. |

| Beneficiaries | A broad class of potential beneficiaries (e.g., family members). | Unitholders with a defined ownership stake. |

| Best Use Case | Family businesses, asset protection, and estate planning. | Joint ventures, property investments with unrelated parties. |

| Flexibility | High degree of flexibility in managing distributions. | Low flexibility; entitlements are locked in. |

Ultimately, the choice between a discretionary and a unit trust really boils down to your specific situation. The best place to start is by asking one simple question: are you managing assets for your family, or are you going into business with partners? Your answer will almost always point you in the right direction.

Getting Your Trust Deed and Legal Status Right

Okay, you’ve decided on the type of trust that fits your situation. Now it’s time to get down to the brass tacks and make it legally real. This is where we move from planning to action, creating the core documents and getting all the official registrations sorted. Getting these details right from the very beginning is absolutely critical for a valid, working trust.

The single most important document you’ll create is the trust deed. You can think of it as the constitution or rulebook for your trust. It’s a legally binding document that spells out the rules, powers, and obligations for everyone involved, and it will govern how the trust operates for its entire life.

Crafting the All-Important Trust Deed

A trust deed isn’t some off-the-shelf template you can just fill in. It has to be carefully drafted to match your specific goals and circumstances. Australian law is very particular about the legal steps for setting up a trust, and the deed is the cornerstone of the whole structure.

A solid trust deed needs to clearly define a few key things:

- The Trustee’s Powers: This part outlines exactly what the trustee can and can’t do with the trust’s assets, from making investments to paying out income.

- Beneficiary Classes: It clearly identifies who is allowed to benefit from the trust. For a family trust, this usually includes spouses, kids, grandkids, and even related companies or other trusts.

- Distribution Rules: The deed must specify how income and capital can be distributed amongst the beneficiaries.

- Vesting Date: This is the expiration date when the trust legally has to end. In Australia, this is typically set for 80 years from the date it was created.

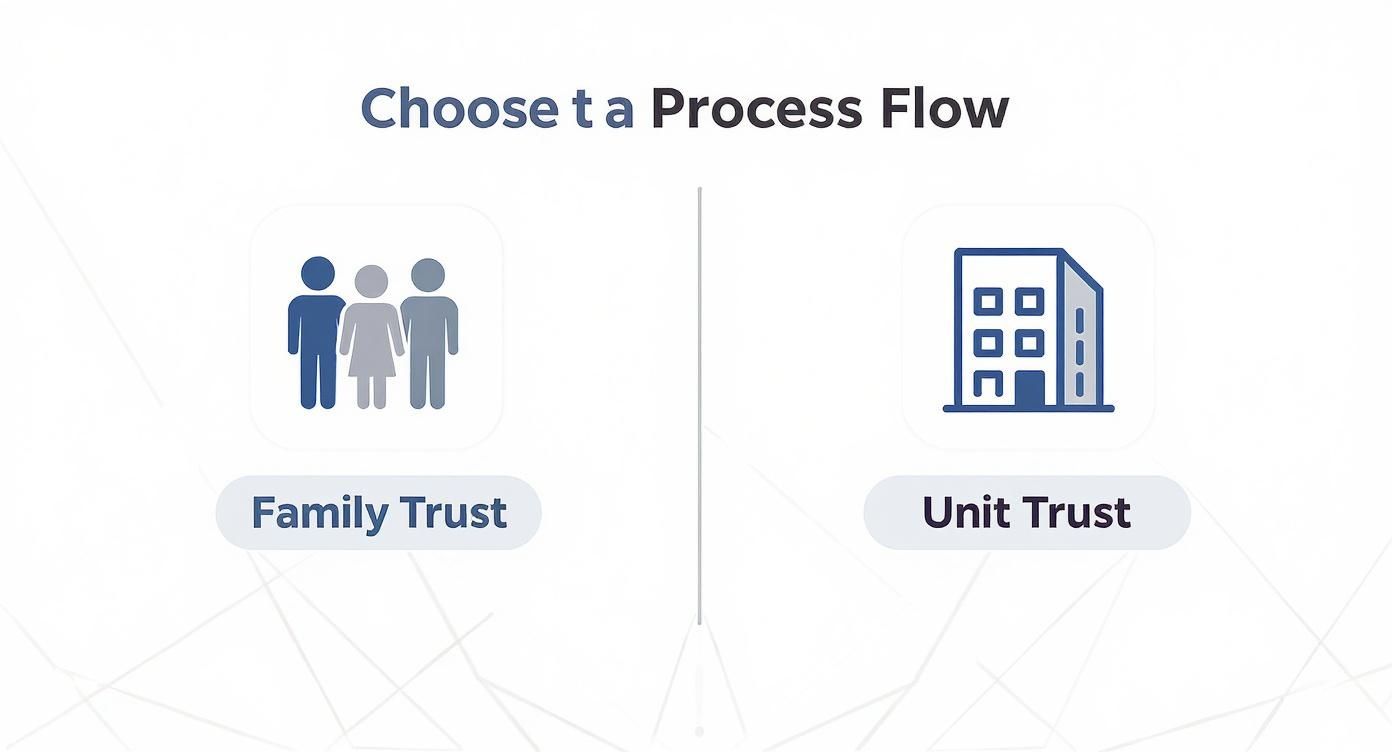

This infographic gives you a quick visual breakdown of the key differences between the two most common trust setups for business owners.

As you can see, family trusts are built for flexible wealth management within a family, while unit trusts are designed for clear, fixed ownership stakes between business partners.

Settling the Trust: The First Official Step

Once the trust deed is drafted and signed by the trustee, the next move is to ‘settle’ the trust. This sounds complex, but it’s a small but legally essential action where the settlor (the person who creates the trust) gives an initial sum of money to the trustee.

This settled sum is usually just a token amount, often $10, but this simple transfer is what officially brings the trust into existence. This money becomes the very first asset of the trust, and it’s vital that this transaction is properly documented.

With the trust settled, the deed then has to be stamped by the relevant state or territory revenue office. Be aware that every state has different rules and fees for this, so you’ll need to check the local requirements. Once it’s stamped, your trust is legally formed. Congratulations!

Getting Registered with the ATO

A legally formed trust is great, but to actually operate, it needs to be on the Australian Taxation Office’s (ATO) radar. This final step makes your trust official in the eyes of the tax system, allowing it to function as a business or investment vehicle.

You’ll need to apply for two key things:

- A Tax File Number (TFN): Just like you have a personal TFN, your trust needs its own unique TFN to lodge its annual tax returns.

- An Australian Business Number (ABN): If the trust is going to run a business or enterprise, an ABN is a must-have. You’ll need it to deal with other businesses and to register for GST if your turnover requires it.

Trying to navigate the fine print of trust deeds and ATO registrations can feel like a maze. If you want to make sure your trust is set up correctly in Australia from day one, it might be worth booking a free consultation to talk through your specific needs with an expert.

Understanding Your Legal Duties as a Trustee

Stepping into the role of a trustee isn’t just about holding a title; it’s a serious legal commitment. You’re taking on a position of immense responsibility, and it’s governed by a strict set of duties designed to protect the beneficiaries. Getting your head around these obligations is the first step to managing the trust effectively and protecting yourself from personal liability.

Your number one job is to act honestly and always in the best interests of all beneficiaries, not just one or two. This is what’s known as a fiduciary duty, and it’s the foundation for every single decision you’ll make, from day-to-day admin to bigger investment strategies. Think of it less as a guideline and more as a non-negotiable legal requirement.

Core Fiduciary Responsibilities

Your duties are laid out in two places: the trust deed itself and general trust law. While the deed might tweak some responsibilities, there are a few core duties that apply to every trustee in Australia. You can’t get around them.

Here are the big ones:

- Acting with Care and Diligence: You need to manage the trust’s affairs with the same level of care that any sensible business person would use for their own money. This means doing your homework and making well-researched, prudent decisions, especially when it comes to investments.

- Avoiding Conflicts of Interest: Your personal interests have to take a backseat. You can’t profit from your role (unless the trust deed specifically says you can be paid) or get into a situation where your needs are competing with the beneficiaries’.

- Acting Impartially: You have to treat every beneficiary fairly. You can’t play favourites, unless the trust deed specifically instructs you to prioritise one beneficiary over another.

A classic mistake I see new trustees make is mixing trust funds with their own personal or business money. It’s a huge no-no. The trust’s property must be kept completely separate, always. Failing to do this is a serious breach of your duties.

Day-to-Day Administrative Tasks

Beyond the high-level principles, being a trustee involves a lot of hands-on, practical work. Good administration is the backbone of any well-managed trust and is absolutely critical for meeting your legal obligations when you set up a trust in Australia.

Your regular admin tasks will include:

- Keeping Meticulous Records: You are legally required to keep spotless, accurate records of everything the trust does financially. We’re talking about all income, expenses, assets bought and sold, and any distributions made to beneficiaries.

- Making Sound Investment Decisions: It’s on you to invest the trust’s assets wisely. This doesn’t mean you have to be totally risk-averse, but your investment strategy must be suitable for the trust’s goals and what the beneficiaries need.

- Informing Beneficiaries: Beneficiaries have a right to know what’s going on with the trust’s assets and management. You need to be ready to provide them with information and explain your actions if they ask.

At the end of the day, your role boils down to one thing: protecting and growing the trust’s assets for the sole benefit of the beneficiaries. Just remember, this guide is for educational purposes—it’s no substitute for getting professional legal advice tailored to your situation.

Managing Ongoing Tax and Compliance

Once you’ve navigated setting up your trust, the work doesn’t stop—it just changes. Your focus now shifts from establishment to the ongoing management and annual upkeep required to keep everything running smoothly and legally.

Think of it like regular car maintenance. You wouldn’t drive for years without an oil change or a service, and the same principle applies here. Skipping these yearly check-ups for your trust can lead to some seriously expensive problems down the track. This annual maintenance cycle revolves around two key jobs: lodging the tax return and handling income distributions correctly.

The Annual Tax Return and Income Distribution

Every financial year, your trust needs to lodge its own tax return with the Australian Taxation Office (ATO). This is where you’ll detail all the income the trust has earned and any expenses it has claimed. Because trusts are such a common structure for managing wealth in Australia, the ATO has specific rules about how their income is taxed—either in the hands of the beneficiaries who receive it or, in some cases, the trustee.

But before you can even think about lodging the tax return, a critical decision needs to be made about how the trust’s net income for the year will be distributed among the beneficiaries. This isn’t a casual chat or a handshake deal; it has to be formally documented.

The Critical June 30 Deadline

If there’s one date you circle in red on the calendar, it’s 30 June. Before midnight on the last day of the financial year, the trustee is legally required to prepare and sign a trustee resolution. This is the formal document that locks in your decisions on which beneficiaries will receive what portion of the trust’s income.

Failing to create and sign this resolution before the 30 June deadline can have serious consequences. If any income has not been properly allocated to a beneficiary, it is considered “undistributed.” This income may then be taxed in the hands of the trustee at the highest individual marginal tax rate, plus any applicable levies.

This isn’t a slap on the wrist; it’s a punitive tax rate designed to ensure trustees distribute income properly each year. Missing this deadline is one of the costliest—and most avoidable—mistakes a trustee can make.

Staying on top of your annual duties is absolutely fundamental. You can explore more articles on our blog to better understand your ongoing tax and compliance responsibilities.

Remember, this information is for general guidance and does not constitute professional tax advice.

Common Questions About Australian Trusts

As you start digging into how trusts work in Australia, a few key questions always seem to come up. It’s completely normal. To help clear things up, I’ve put together some straightforward answers to the queries we hear most often from business owners just like you.

Just remember, this is general info to help you get your head around the common sticking points. It’s no substitute for getting professional legal or financial advice that’s shaped around your specific situation.

How Much Does It Cost to Set Up a Trust in Australia?

The cost to set up a trust can really swing from one end of the scale to the other. You’ll see basic online templates advertised for a few hundred dollars, but a properly customised trust deed drafted by an experienced solicitor could run into several thousand.

What you end up paying really comes down to how complex your financial life is and what you want the trust to achieve. A more detailed structure built for serious asset protection is naturally going to have a higher upfront cost than a simple family trust. Don’t forget to factor in the ongoing costs too, like annual accounting fees to keep everything compliant.

Can I Be Both a Trustee and a Beneficiary?

Yes, absolutely. This is actually a very common setup, especially in discretionary or family trusts where a parent might be the trustee (or director of the corporate trustee) and also one of the potential beneficiaries.

The big catch here is that this dual role demands you be incredibly careful about conflicts of interest. As a trustee, your legal duty is to act in the best interests of all beneficiaries as a group, not just yourself. Every single decision has to be impartial and well-documented.

What Happens if Trust Income Is Not Distributed by June 30?

This is a critical deadline that trips up a lot of new trustees, so pay close attention. If the trust has any net income for the financial year left sitting in its bank account after the 30 June deadline, the Australian Taxation Office (ATO) gets involved.

Any of that undistributed income may be taxed directly in the hands of the trustee at the highest individual marginal tax rate, plus any levies on top. It’s a painful tax bill designed as a powerful incentive to make sure trustees sort out their paperwork and sign a resolution to distribute all the income before the clock strikes midnight on June 30.

Is It Necessary to Hire a Lawyer to Set Up a Trust?

While there’s no law that says you must use a lawyer, it is highly recommended. Think of the trust deed as the constitution for your financial structure. Even tiny errors or vague wording in that document can cause massive headaches down the line.

An improperly drafted deed could lead to the whole trust being declared invalid, create unexpected tax problems, or completely fail to give you the asset protection you were counting on. Bringing in an experienced solicitor from the start ensures your trust is legally solid, set up correctly, and genuinely fit for purpose. It’s an investment in peace of mind.

Navigating the world of trusts requires expert guidance to get it right. The team at Genesis Hub provides clear, practical advice to help small business owners establish and manage their financial structures correctly. For proactive support that strengthens your business performance, visit us at Genesis Hub.