The big trade-off with the sole trader structure really boils down to one thing: simplicity versus risk. On one hand, it's incredibly simple and cheap to set up. On the other, you have unlimited personal liability, which means your personal assets are on the line if the business gets into debt. Getting your head around this balance is the first step for anyone considering this path in Australia.

What Is a Sole Trader in Australia

A sole trader is the most straightforward business structure you can choose in Australia. Essentially, you are the business. There's no legal separation between you as an individual and your commercial activities.

This means you call all the shots, you keep all the profits, and you’re personally on the hook for any debts the business racks up. You'll operate using your personal Tax File Number (TFN) to report your income, but you’ll also need an Australian Business Number (ABN) for all your business dealings.

It’s this flexibility that makes it a go-to for so many freelancers, contractors, and people just starting out. It's no surprise that a huge chunk of Australian businesses are non-employing—in fact, 62.5% fit this description, and that includes a massive number of sole traders. You can dig deeper into the makeup of Australian small businesses to see the stats for yourself.

Sole Trader At a Glance Key Pros and Cons

To really get to the heart of it, let's lay out the main pros and cons side-by-side. This table cuts through the noise and shows you the fundamental trade-offs you're making.

| Aspect | Key Advantage | Key Disadvantage |

|---|---|---|

| Legal Structure | Simple and Inexpensive Setup: Minimal paperwork and low startup costs. | Unlimited Personal Liability: Your personal assets can be used to cover business debts. |

| Control & Profits | Full Autonomy: You make all decisions and retain 100% of the profits. | Sole Responsibility: You bear the full weight of all business risks and decisions. |

| Administration | Lower Compliance Burden: Fewer reporting requirements compared to a company. | Limited Growth Potential: Can be harder to secure large-scale investment or loans. |

Seeing it laid out like this makes the core decision pretty clear: Are you willing to accept greater personal risk in exchange for maximum simplicity and control? Your answer to that question will tell you if the sole trader path is the right one for you.

Key Advantages of the Sole Trader Model

So, why do so many Aussie entrepreneurs kick off their journey as a sole trader? It really boils down to a few core benefits: it’s simple, you’re in complete control, and the administrative headaches are much smaller. For anyone just starting out, this can be a massive drawcard.

One of the biggest wins is just how fast you can get up and running. Once you’ve registered for an Australian Business Number (ABN) — a process that’s typically quick and cheap — you can pretty much start trading straight away. This means you can go from a great idea to a functioning business much faster than it takes to set up a company.

Unmatched Control and Financial Simplicity

As a sole trader, you're the boss. Period. Every decision is yours to make, from big strategy pivots to small pricing tweaks. There are no shareholders to please or board meetings to schedule, giving you the freedom to act fast. This is a huge advantage.

Imagine a freelance graphic designer who decides overnight they want to specialise in a new software. As a sole trader, they just do it. No approval needed. All the profits you make are yours to keep, and the bookkeeping, at least initially, is often far less complicated than a company's. While getting professional advice is always a smart move, you can find out more on why in our guide about the top reasons small businesses should work with a tax accountant.

The ability to retain all profits and make unilateral decisions offers a level of agility that more complex business structures simply cannot match, allowing for rapid adaptation to market changes.

Lower Costs and Greater Privacy

It’s not just quicker to set up a sole trader business; it’s also cheaper to run. The ongoing costs for compliance and admin are significantly lower than what you’d face with a company structure. This frees up precious cash that you can pump back into growing your business.

On top of that, sole traders get to keep things a bit more private. Companies have public records showing who the directors and shareholders are. As a sole trader, your business and financial information doesn’t have to be publicly disclosed. For many business owners who prefer to keep their operations under the radar, this is a real plus.

Understanding the Risks and Disadvantages

While the simplicity of being a sole trader is a massive drawcard, it’s absolutely critical to weigh this against the significant downsides. You have to get a balanced view of the risks before you commit, as this structure carries responsibilities that can directly impact your personal financial security.

The single biggest drawback is unlimited personal liability. As a sole trader, the law makes no distinction between you and your business. This means if your business racks up debts it can’t pay, your personal assets—your home, car, and savings—are on the line to settle those debts. For many people, this personal exposure is the dealbreaker. The self-employed workforce in Australia is substantial, but this risk is a constant reality for every one of them.

The Challenge of Liability and Perception

Let’s put that in real-world terms. Imagine you're a tradesperson and a client successfully sues you for property damage. If your business insurance doesn't cover the full amount, creditors can come after your personal assets to make up the difference.

This fusion of personal and business identity means every business risk is also a personal financial risk. Unlike a company structure, there is no corporate veil to protect your personal wealth from business liabilities.

Another challenge is just how you're perceived. In some industries, clients and suppliers see a registered company as a more established and credible operation. This can sometimes make it harder for a sole trader to land bigger contracts or build trust with larger corporate partners, putting a potential ceiling on your growth.

Limitations on Capital and Business Continuity

Accessing capital is another major hurdle. Trying to get a large business loan or attract investment is often much harder when your business’s financial identity is tangled up with your personal wealth. Banks can see this as a higher risk, which might limit your ability to fund expansion. Managing what you take from the business is also vital; our guide offers detailed insights on handling owner's drawings for your small business.

Finally, the business has no real life of its own. A sole trader business can't be sold as a standalone entity in the same way a company can, because its existence is tied directly to you. If you retire or can no longer work, the business effectively disappears with you.

Sole Trader vs Company: A Head-to-Head Comparison

Choosing your business structure is one of the first, and most critical, decisions you'll make. The sole trader path offers beautiful simplicity, but you absolutely have to weigh that against the protection and growth potential of a proprietary limited (Pty Ltd) company. Each structure comes with a very different set of trade-offs.

A company is a separate legal entity from you, the owner. This is the fundamental difference, creating a vital barrier between your business and personal finances. For a sole trader, that barrier simply doesn't exist; in the eyes of the law, you and your business are one and the same.

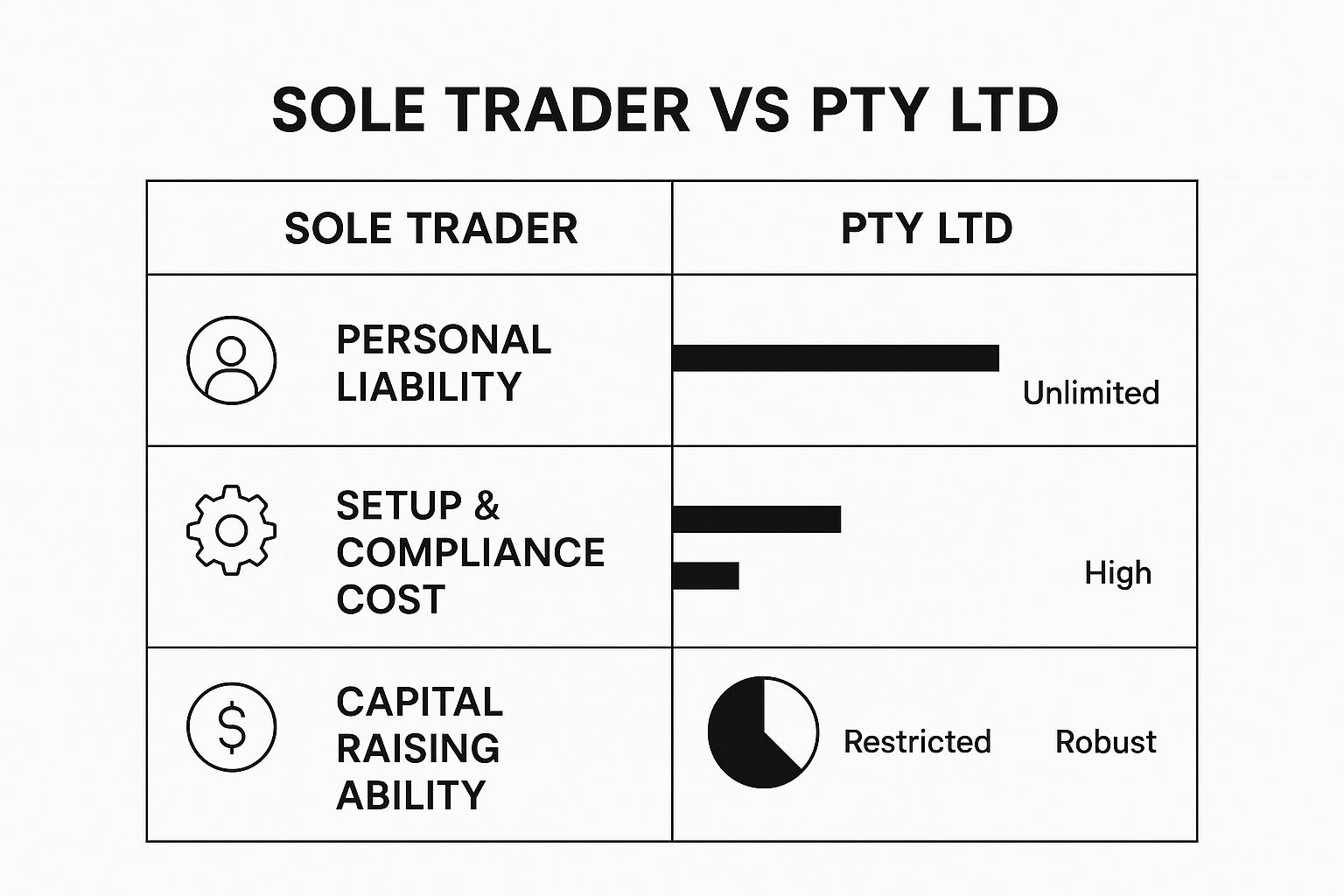

This infographic breaks down the core differences in a really clear way.

You can see the inverse relationship at a glance. Sole traders get the benefit of low costs and simple setup, but that comes with unlimited personal liability and a tough time raising funds. Companies face higher costs and more paperwork but gain that all-important liability protection and far better access to capital.

Let’s dig into what this means in the real world with a side-by-side comparison.

Comparing Sole Trader and Company Structures

This table breaks down the key distinctions between these two common business structures in Australia, helping you see where your priorities might lie.

| Feature | Sole Trader | Company (Pty Ltd) |

|---|---|---|

| Legal Status | You and the business are a single legal entity. | A separate legal entity from its owners (shareholders). |

| Liability | Unlimited personal liability. Your personal assets are at risk. | Limited liability. Personal assets are generally protected from business debts. |

| Taxation | Profits are generally taxed as part of your individual income. | A company pays tax on its profits at the corporate tax rate. |

| Setup Cost & Complexity | Simple and inexpensive. Just need an ABN. | More complex and costly to set up and maintain (ASIC fees). |

| Ongoing Compliance | Minimal. Lodge your personal tax return with a business schedule. | Higher. Requires annual reviews, director duties, and separate tax returns. |

| Raising Capital | Difficult. Relies on personal savings or personal loans. | Easier. Can issue shares to investors to raise capital for growth. |

| Business Name | Your personal name, or you can register a business name. | Must register a unique company name with ASIC. |

Choosing the right structure really comes down to your personal risk tolerance, your business goals, and how much complexity you're willing to take on.

Liability and Asset Protection

This is the big one. The most significant advantage of operating as a company is limited liability. If the business racks up debts it can't pay, your personal assets—like your family home—are generally protected.

As a sole trader, you have unlimited liability. This means your personal assets could be on the line to settle business debts. It's a critical risk you need to be comfortable with.

Choosing a company structure separates your business's financial fate from your personal financial security. For a sole trader, these two are legally intertwined, making every business risk a personal one.

Raising Capital and Growth Potential

Another major hurdle for sole traders is getting access to capital. You're often relying on your own savings or a personal loan to get things off the ground, which can seriously limit how much you can invest in growth.

As businesses get bigger, they need more sophisticated funding options. You can discover more insights about small business funding and the challenges involved.

A company can issue shares to bring in new investors, making it much easier to raise serious capital for expansion. For a sole trader, that path just isn't available, which can put a cap on your long-term ambitions.

When Does Being a Sole Trader Make Sense?

Picking the right business structure isn't just a box-ticking exercise; it's about matching the way you operate with your personal situation and future goals. The sole trader model, with all its pros and cons, is a fantastic fit for certain situations, especially when you're just getting your feet wet.

For anyone in the freelance, independent contractor, or gig economy world, the sole trader setup is practically the default choice—and for good reason. It’s cheap to set up and the formalities are minimal, which means you can start earning money fast without getting bogged down in the administrative headaches of running a company. If you're a graphic designer, a ride-share driver, or a consultant, this simplicity lets you pour your energy into your actual work, not endless compliance.

Ideal Scenarios for Sole Traders

This structure is also tailor-made for entrepreneurs looking to test out a new business idea. Let's say you're launching a small online store or a local service where the initial risks are low. Operating as a sole trader lets you prove your concept without a huge upfront financial commitment. You get to test the waters, see if people are interested, and build a customer base before you even think about moving to a more complex and expensive structure.

It's also a really practical choice for small, low-risk businesses where the chances of a major liability claim are pretty slim. A home-based baker or a private tutor, for instance, just doesn't face the same level of risk as a construction business.

The sole trader structure is a powerful starting point, but the right choice depends on aligning the structure's risks and benefits with your current business reality and future ambitions.

Ultimately, your decision has to come down to your personal tolerance for risk and your long-term vision. As your business starts to grow, your finances will inevitably get more complicated. That's when understanding why every business needs an accountant can give you the critical clarity you need to plan your next move.

A Few Common Questions About Being a Sole Trader

Even after laying out all the pros and cons, you’re probably still mulling over a few practical questions. It’s completely normal. Let's tackle some of the most common queries that pop up once you start thinking about the day-to-day realities of being a sole trader.

Can a Sole Trader Hire Employees?

Absolutely. There's nothing stopping you from hiring staff as a sole trader. But, and this is a big but, the moment you become an employer, you step into a world of new legal responsibilities.

Taking on employees isn't just about paying wages. You're legally required to manage:

- PAYG Withholding: This means you have to withhold tax from your employees' pay and send it off to the ATO.

- Superannuation: You must pay super contributions into your employees' nominated funds. In Australia, this is a non-negotiable part of being an employer.

- Workers' Compensation: You’ll also need to arrange the right insurance to cover your team in case of any workplace injuries.

Getting this right from day one is critical. These obligations add another layer of admin to your business, so it's something to be prepared for.

What Happens if My Sole Trader Business Fails?

This is where the concept of 'unlimited liability' really hits home. If the business doesn't make it, there’s no legal distinction between you and the business entity. You are personally on the hook for any and all outstanding debts.

This is the single biggest risk for a sole trader. Creditors can pursue your personal assets—like your home or car—to settle business debts if the business itself can't pay. It’s a financial risk that extends well beyond your business bank account.

Winding up the business is also a formal process. It’s not just a matter of closing your doors. You have to notify the ATO and make sure your ABN is cancelled to properly finalise all your obligations.

How Do I Switch from a Sole Trader to a Company?

Making the jump from a sole trader to a company is a very common path for a growing business. It’s often the logical next step when you want to protect your personal assets from liability or need to bring in investors.

The process involves registering a new company with ASIC and then formally transferring your business assets over to this new legal entity.

This is a major structural change, not just a bit of paperwork. It’s highly recommended that you get professional legal and financial advice to make sure the transition is handled correctly, covering all the tax and legal bases.

Navigating these questions is much simpler with an expert on your side. At Genesis Hub, we specialise in helping sole traders manage their financial obligations and plan for growth. Book your free consultation with Genesis Hub to get clear, practical advice for your business journey.